Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

Just when we think the market is becoming more rational and beginning to focus on fundamentals again we find a stock that proves that idea wrong. Once again, we’ve identified a business that fails to generate profits, uses “adjusted” metrics as “better representations of business”, and who’s stock price is up over 200% since late 2012. ServiceNow (NOW: $81/share) is in the Danger Zone this week.

Revenue Growth At The Expense Of Profit

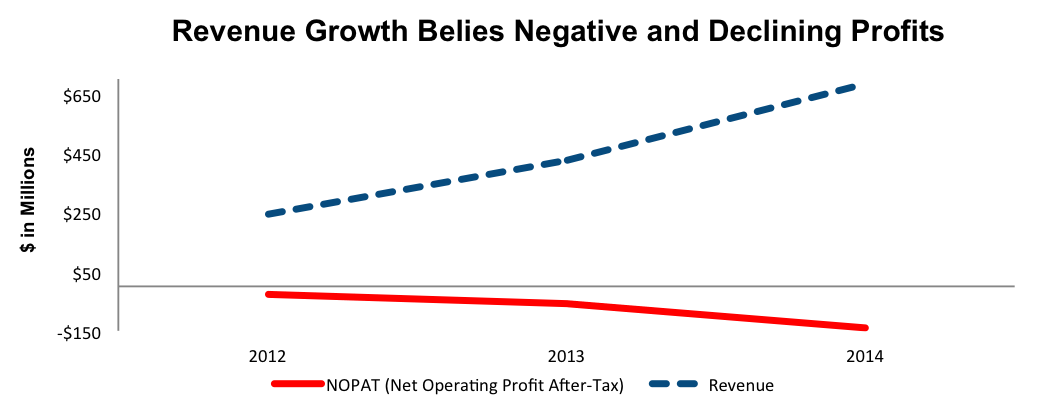

ServiceNow was founded in 2004 with the goal of managing and automating any number of information technology tasks in which enterprises may engage in day-to-day operations. As much as these services benefit clients, they do not serve the business or investors well. Figure 1 shows that despite strong revenue growth, ServiceNow’s after-tax profits (NOPAT) have declined from -$30 million in 2012 to -$166 million on a trailing twelve-month (TTM) basis.

Figure 1: Revenues Fail To Be Converted Into Profits

Sources: New Constructs, LLC and company filings

Costs Growing Much Faster Than Revenues

While revenues have grown at 67% compounded annually since 2012, sales & marketing, research & development, and general & administrative costs have grown at 81%, 94%, and 68% compounded annually respectively since 2012.

ServiceNow’s return on invested capital (ROIC) has followed the downward trend in profits and has declined from -28% in 2012 to its current bottom quintile -74% on a TTM basis.

We’ve seen this trend before in other cloud companies that we’ve also put in the Danger Zone: Marketo (MKTO), Proofpoint (PFPT), and Demandware (DWRE). Collectively, those three stocks are down an average -2% versus the S&P at +3% since they were put in the Danger Zone.

Adjusted Performance Metrics Help Execs At Expense of Investors

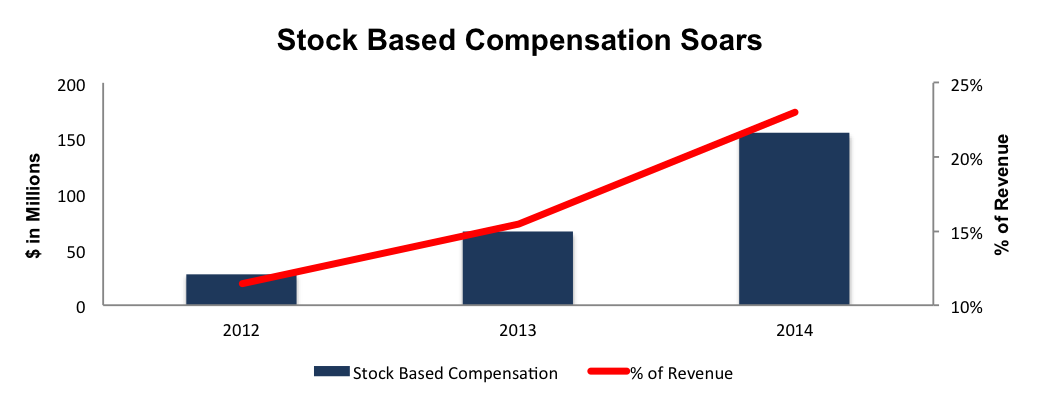

But wait how can this be? ServiceNow’s management directs attention to metrics that look good, for example: increasing annual contract values, growing billings, and excellent gross margins. What investors have failed to recognize, or chosen to ignore, is that these metrics divert focus off of the business’ increased losses. Even worse, the gross margin that ServiceNow highlights is calculated on a non-GAAP basis, a big red flag. What is the biggest adjustment made to arrive at NOW’s non-GAAP metrics? Removing stock based compensation (23% of revenue in the last fiscal year). Figure 2 shows the magnitude of this “adjustment”.

Figure 2: ServiceNow’s Stock Based Compensation

Sources: New Constructs, LLC and company filings

Since 2012, ServiceNow’s stock based compensation has grown from $27.9 million to $154.3 million in 2014. These costs represented 11% of revenue in 2012 and 23% of revenue in 2014. Don’t rely on adjusted numbers as they fail to present the true picture.