What do McDonald’s (MCD), Philip Morris (PM), Caterpillar(CAT), Kimberly-Clark (KMB), and Target (TGT) have in common?

Yes, they’re all large-cap stocks that pay solid dividends.

In fact, three are even Dividend Aristocrats, having increased their dividends for at least 25 consecutive years.

But the common characteristic I’m referring to isn’t related to their dividends… or even their common stocks. Instead, I’m looking higher up in the capital structure.

Specifically, each of the above companies is rated single-A by Standard & Poor’s, a major credit ratings agency.

They may not be AA- or AAA-rated, but single-As still have excellent credit worthiness, and tend to have narrow credit spreads (the additional yield provided by a corporate bond above that of U.S. Treasuries to compensate investors for the risk of default).

At the moment, though, credit spreads for investment-grade (IG) corporate bonds are actually widening.

For their part, many market watchers are quick to dismiss the selloff in high-yield bonds, attributing it solely to the turmoil in the energy sector. But this is a mistake in its own right.

Meanwhile, the companies I’ve mentioned are a far cry from super-speculative, highly leveraged oil exploration and production firms.

Indeed, high-quality bonds have started selling off, too, and most are outside of the energy sector.

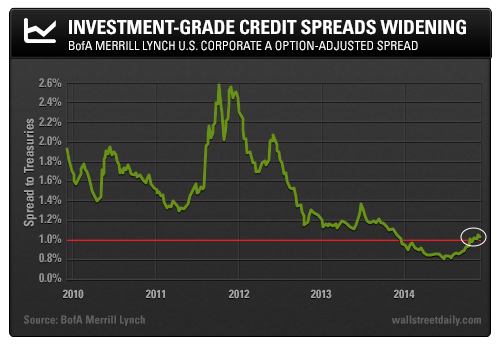

After spending the majority of 2014 below 1% (100 basis points), benchmark single-A credit spreads have now pierced this key level, as you can see below:

Heading into 2015, there are two important takeaways from the action in IG credit spreads: