In this paper I want to explain the readers how the Maximum Yield Rotation Strategy of Logical Invest is built. This Strategy achieves very high returns investing in inverse volatility. From 2011 to today the annual performance was more than 50% per year. The Sharpe Ratio (Return/Risk) of 2.04 is a “DREAM VALUE” and I doubt that someone can show me a strategy with a higher ratio.

The strategy invests in 4 different ETFs:

The Maximum Yield Strategy switches semi-monthly between these 4 ETFs. For the switching I use a ranking system like the one I explained in my Global Market Rotation Strategy article in 2013. The ranking system is also using 3-month historical performance and 20 day volatility. Using volatility is quite important, because it reduces the ranking of high volatile ETFs like ZIV.

However, if you want to play such a rotation strategy by yourself, then you can also just look at the 3-month historical performance.

In this strategy the ZIV ETF is the most important performance driver. ZIV can only be backtested since 2011, so that I cannot present a longer backtest for the whole strategy, but the way the strategy is built, you can backtest parts of it for more than 10 years.

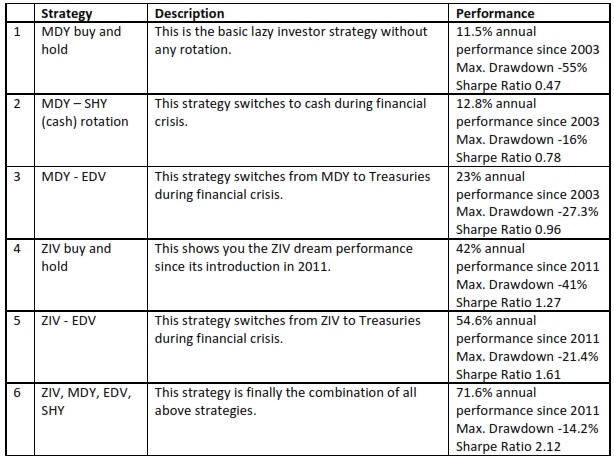

The Maximum Yield Rotation Strategy is composed of several smaller sub-rotation strategies. Here is an overview of these different strategies:

Here are some comments to the above strategies: