Here’s the story in a nutshell: Ultra low interest rates mark a shift away from people’s wealth residing in their savings and pension plans, and into to so-called wealth residing in their homes, which are bought with ever growing levels of debt. When interest rates rise, they will lose that so-called wealth.

It is grand theft auto on an unparalleled scale, and it’s a piece of genius, because while people are getting robbed in plain daylight, they actually think they’re winning. But as I wrote back in March of this year, home sales, and bubbles, are the only thing that keeps our economies humming.

We haven’t learned a thing since March, and we haven’t learned a thing for many years. People need a place to live, and they fall for the scheme hook line and sinker. Which in a way is a good thing because the economy would have been dead without that ignorance, but at the same time it’s not because it’s a temporary relief only and the end result will be all the more painful for it.

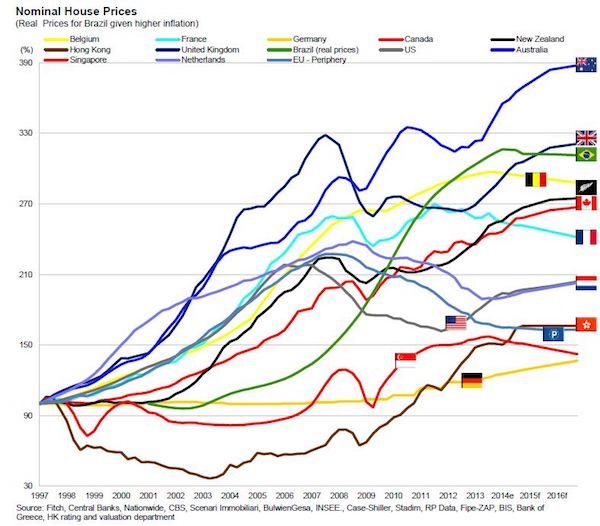

Whatever Yellen decides as per rates, or Draghi, it doesn’t really matter anymore, this sucker’s going down something awful. This is a global issue. Housing bubbles have been blown not only in the Anglosphere, though they are strong there, many other countries have them as well, Scandinavia, Netherlands, even Germany, and France. It’s what ultra low rates do.

First, here’s what I said in March:

Our Economies Run On Housing Bubbles

What we have invented to keep big banks afloat for a while longer is ultra low interest rates, NIRP, ZIRP etc. They create the illusion of not only growth, but also of wealth. They make people think a home they couldn’t have dreamt of buying not long ago now fits in their ‘budget’. That is how we get them to sign up for ever bigger mortgages. And those in turn keep our banks from falling over.

Record low interest rates have become the only way that private banks can create new money, and stay alive (because at higher rates hardly anybody can afford a mortgage). It’s of course not just the banks that are kept alive, it’s the entire economy. Without the ZIRP rates, the mortgages they lure people into, and the housing bubbles this creates, the amount of money circulating in our economies would shrink so much and so fast the whole shebang would fall to bits.

That’s right: the survival of our economies today depends one on one on the existence of housing bubbles. No bubble means no money creation means no functioning economy.

What we should do in the short term is lower private debt levels (drastically, jubilee style), and temporarily raise public debt to encourage economic activity, aim for more and better jobs. But we’re doing the exact opposite: austerity measures are geared towards lowering public debt, while they cut the consumer spending power that makes up 60-70% of our economies. Meanwhile, housing bubbles raise private debt through the -grossly overpriced- roof.

This is today’s general economic dynamic. It’s exclusively controlled by the price of debt. However, as low interest rates make the price of debt look very low, the real price (there always is one, it’s just like thermodynamics) is paid beyond interest rates, beyond the financial markets even, it’s paid on Main Street, in the real economy. Where the quality of jobs, if not the quantity, has fallen dramatically, and people can only survive by descending ever deeper into ever more debt.

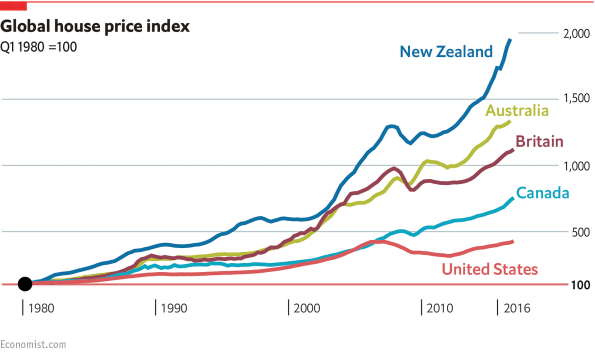

Australia’s housing boom has been a thing of beauty, with New Zealand, especially Wellington and Auckland, following close behind. UBS now says the Oz bubble is over. Prices are still rising quite a bit though.