Thursday’s ECB meeting is expected to be one of the most important in recent years: Mario Draghi has signaled, and is widely expected to announce a blueprint of what the central bank’s QE tapering will look like beyond 2017, and while no actual tightening will be implemented – either via rates of asset purchases – the ECB is expected to announce it will cut its €60bn/month bond purchases in roughly half starting in January 2018 and lasting for the next 9-15 months.

Courtesy of RanSquawk, here are the key parameters of Thursday’s meeting:

Rate Decision due at 1245BST/0645CDT and Press Conference at 1330BST/0730CDT

The ECB is widelyexpected to keep all rates on hold, with rate hikes not expected until after conclusion of current QE programme

The ECB is expected to unveil a road-map for reducing the pace of asset purchases given rhetoric from Draghi at the previous press conference

Consensus far from clear on how much the ECB will reduce purchases by and how long they will be extended for

RATE/ASSET PURCHASE EXPECTATIONS

DEPOSIT RATE: Forecast to remain unchanged at -0.40%. The rate was last adjusted in March 2016, when it was cut by 10bps.

REFI RATE: Forecast to remain unchanged at 0.00%. The rate was last adjusted in March 2016, when it was cut by 5bps.

MARGINAL RATE: Forecast to remain unchanged at 0.25%. The rate was last adjusted in March 2016, when it was cut by 5bps.

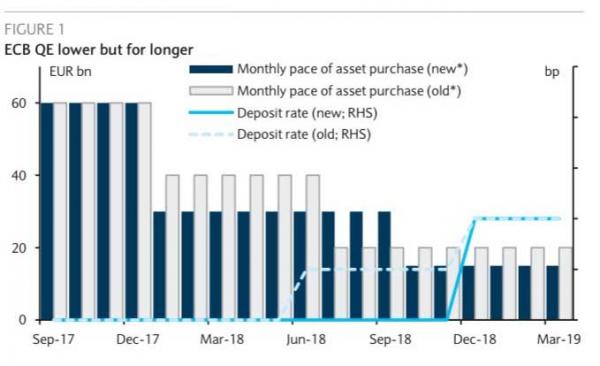

ASSET PURCHASES: Views on this front are particularly wide-ranging. A Reuters poll suggests that the ECB will start trimming monthly asset purchases to EUR 40bln from current EUR 60bln in January. Views are mainly split onwhether this will be via a 6- or 9-month extension. However, Bloomberg News reports that the Bank will half purchases to EUR 30bln (a view backed by recent source reports) while extending the programme by 9-months in order to take the total size of purchases to around EUR 2.5trl; a level seen by some as their maximum purchase limit. (Discussed in greater detail later on in the report)

CURRENT ECB FORWARD GUIDANCE

RATES: “We expect [rates] to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.” (ECB statement, 7/Sept)

ASSET PURCHASES: “Net asset purchases, at the current monthly pace of EUR 60bln, are intended to run until the end of December 2017, or beyond, if necessary” (ECB statement, 7/Sept)

GROWTH: “The risks to the growth outlook are broadly balanced.” (ECB statement, 7/Sept)

INFLATION: “While the ongoing economic expansion provides confidence that inflation will gradually head to levels in line with our inflation aim, it has yet to translate sufficiently into stronger inflation dynamics. Measures of underlying inflation have ticked up slightly in recent months but, overall, remain at subdued levels. Therefore, a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up and support headline inflation developments in the medium term.” (ECB statement, 7/Sept)

POTENTIAL ADJUSTMENTS TO ECB FORWARD GUIDANCE

RATES: Expected to stick to current rhetoric with any adjustments on rates not expected until QE unwind as part of their ‘sequencing’ efforts.

ASSET PURCHASES: This will hinge on what action the ECB will take. (Expectations for this are discussed below).

GROWTH: No change to guidance expected on this front. RBC states there has been little in the way of economic data flows to materially alter the economic backdrop.

INFLATION: Similarly to the growth story, little has changed on the inflation front to require any adjustment to current guidance.

FUTURE PATH OF QE PROGRAMME

Background:

Despite inflation in the Euro-area (1.5% Y/Y headline) still short of the ECB’s ‘close to but below 2%’ target, the Bank has

found itself under pressure to set out a road-map on how they will curtail purchases. This is a by-product of a pick-up

in Euro-area sentiment and growth expectations but more pertinently, the concerns on the governing council surrounding the

Bank moving ever closer to their alleged self-imposed purchase limit of around EUR 2.5trl (set to reach EUR 2.28trl by yearend)