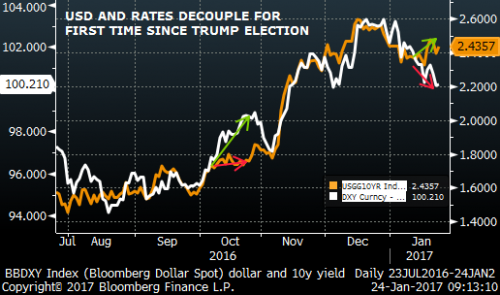

The day the Dow crosses 20,000 may finally be here, because with DJIA futures trading 65 points higher in premarket trading, added to yesterday’s close of 19,912 and latest record high in the S&P, it means that all it will take is a modest of only 25 points for the critical Dow threshold to be finally breached. Celebrating the upcoming record, world stocks hit a 19-month high on Wednesday, lifted by strong Japanese trade data, strong European company earnings and hopes that U.S. President Donald Trump will press ahead with a large fiscal spending package. In short: the Trumpflation rally is back with a bang (even if the dollar is not particularly enjoying it, although the decoupling between the USD and rates was duly noted yesterday so it isn’t too surprising).

“U.S. stocks have shown renewed signs of life this week, as the market toyed with the idea of reigniting the ‘Trump rally’ that we saw in the aftermath of the presidential election,” said Kathleen Brooks, research director at City Index.”Wednesday’s key theme is the return of the ‘Trump trade’,” Brooks said.

In early trading, European equities extended the global rally as corporate earnings reignited investors’ optimism in economic growth with construction companies outperforming on expectations Trump will announce the “massive” Mexican wall.

The MSCI All-Country World Index rose to 433.6, up 02%, to its highest level since June 2015 as equity markets from Tokyo to London climbed after the S&P 500 Index closed at a record. BHP Billiton Ltd. (BHP) paced gains in resources shares and iron ore extended a rally. A surge in industrial metals bolstered raw-materials companies, while gold declined for a second day.The yen edged higher after sliding Tuesday. The Aussie fell after weaker-than-expected inflation data, while oil retreated after a four-day advance.

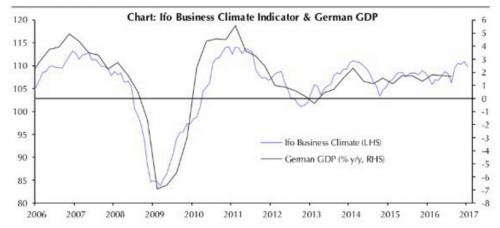

Europe’s index of 300 leading shares and Germany’s DAX both rose 1 percent and Britain’s FTSE 100 was up 0.7 percent.Spanish bank Santander was among the big gainers in Europe, its 4 percent rise in 2016 net profit giving its share price a similar boost and leading the continent-wide rally in bank stocks, despite some disappointing data out of the German IFO survey which missed on both expectations and conditions.

Japan’s Nikkei advanced 1.4 percent, buoyed by data showing the country’s exports rose for the first time in 15 months in December, a positive sign for the economy even as talk of U.S. protectionism looms over the outlook.

Corporate earnings are offering relief after traders began to unwind a rally in the dollar and equities amid concern that gains after Trump’s election had gone too far. Alibaba Group Holding Ltd. lifted its sales forecast as Chinese spending held strong and BHP reported a gain in second-quarter iron ore production after prices soared on demand from China. D.R. Horton Inc., the largest U.S. homebuilder, topped analysts’ estimates as job growth fueled buyer demand. As a result, S&P U.S. futures pointed to a higher open on Wall Street. On Tuesday the S&P 500 and Nasdaq both rose to fresh record highs and the Dow Jones Industrials came within 51 points of the elusive 20,000 mark. On Wednesday, the S&P is poised for another all time high.

Lingering concerns about growing protectionism from the Trump administration, and the potential negative effects on global trade and growth, remained close to the surface.

“It has kept dollar/yen flat despite the S&P 500 hitting new highs and Treasury yields edging up,” Kit Juckes, head of FX research at Societe Generale in London, was quoted by Reuters. “There’s no doubt that a major bout of protectionism-induced risk aversion would be yen-supportive, as well as negative for a bunch of currencies that depend on U.S. trade,” he said.

The 10-year yield inched up to 2.48 percent, recovering from its dip below 2.40 percent earlier in the week, while the two-year yield held firm at 1.23 percent. It was as low as 1.14 percent on Monday. While the greenback moved in tandem with the snap back in U.S. Treasury yields overnight, it struggled to make much headway in Asian and European trading. Germany’s 10-year Bund yield rose to a six-week high of 0.38 percent and France’s benchmark 10-year yield hit a one-year high of 0.95 percent, with bond prices weighed down by the rally in stocks and new debt supply.

The dollar slipped 0.1 percent to 113.65 yen, and 0.1 percent against a basket of currencies. The euro was unchanged at $1.0725, little-moved by a surprised fall in German business morale this month. Sterling jumped, rising just shy of $1.26 on a combination of short covering and position squaring. The decision overall was seen as clearing the way for Prime Minister Theresa May to get on with launching Brexit talks. Sterling has bounced 4 percent over the last week.